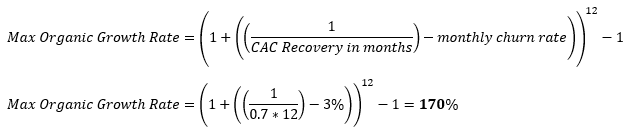

There’s something a bit magical about the LTV:CAC ratio. The idea of “a dime in, a dollar out” is the reason why the SaaS business model is so compelling: to the growth investor, it's the promise of partnering with a businesses into which heaps of CAC dollars can be invested, with the almost certain promise that multiples of those invested dollars will return to the fund and their LPs.

So it seems natural to conclude that the ratio between (fully discounted) LTV, and CAC, or the so-called “LTV:CAC ratio”, is of paramount importance to both SaaS company and their prospective investors (or, indeed, their prospective acquirers). Taking this as a given, then, how important is it to ensure that the ratio is calculated properly, and what might contribute to inaccurate assessments of the same?

Having pored over dozens of SaaS business' income statements, one of the things that jumps out is the allocation of SG&A, or specifically marketing and sales SG&A, between CAC and COGS. According to KBCM (formerly Pacific Crest), the average SaaS business spends 35% of revenue on Sales and Marketing, which is the input basis for total CAC spend. The same cohort of companies allocated 17% to COGS. In a SaaS company, COGS ought to include obvious expenses like hosting, but it should also include any trailing commissions that might otherwise be allocated to SG&A, and all reasonable ongoing customer support costs. COGS should exclude expenses like onboarding and training, unless those are explicitly offset against a separate revenue line item, and should otherwise be allocated CAC, as they are effectively a real and one-time cost associated with the full acquisition of a new customer. This is just one area where a company might be tempted to fiddle with the allocation between COGS and S&M expenses.

Let’s take a look at the implications of moving what ought to be CAC dollars, into COGS. In the two examples below, a $5M ARR B2B SaaS business with a fairly modest $10k average ACV, sports a 20% COGS and spends 30% of their revenue on Sales and Marketing expenses captured as CAC. With a 10% churn and 20% revenue growth targets, and a 25% cost of capital (discount rate), their LTV:CAC ratio is just 2.3:1. Given most investors are willing to take LTV:CAC on an undiscounted but Gross Margin adjusted basis, the ratio would be a less alarming 8:1.

However, if we move just 10% of the CAC burden into COGS, we see the following comparative change:

Fully discounted LTV:CAC jumps to 3:1 and undiscounted up to 10.5:1. It’s comparatively easy to find 10% of your otherwise S&M spend to allocate to COGS, and in many cases it may be a totally legitimate reallocation, even under the auspices of the revised revenue recognition standards detailed in the relatively new ASU 2014-09 and IFRS 15 updates.

The punchline is this: one of the most economically critical SaaS ratios is highly sensitive to the allocation of expenses between the S&M SG&A, and COGS line items. It’s worth having a closer look at this allocation, as a SaaS company CFO, in anticipation of the scrutiny you can be sure to expect from prospective growth investors, or acquirers.

If you’d like an even better intuitive sense of how these numbers relate, please feel free to change the inputs in the interactive calculator, below: